This page is the implementation reference — code excerpts, file structure, design decisions. Useful if you're verifying the methodology is real, planning to clone and run the bridge yourself, or extending it for a different MMM tool.

If you want the buyer-facing pitch, see the Strategy page. For the methodology overview without code, see the Methods page.

Architecture

The bridge is a four-stage pipeline. Each stage takes a structured object from the previous stage, transforms it, and hands it to the next. Components are deliberately decoupled: each can be tested, replaced, or extended independently.

What the bridge adds beyond Robyn

Robyn produces a regression fit. The bridge adds three things the regression doesn't have:

- An explicit

LatentDemandStateconfounder. A root node with arrows to all media channels and to Sales. The back-door Robyn assumes away. Strength is parameterized asλso the analyst can sweep it. - U-noise parents on every substantive node. Required for Rung-3 (counterfactual) inversion via twin networks. Each

U_Xnode is a unit-variance Gaussian root that captures the unexplained variance of its substantive partner. - Linearized media coefficients. Robyn's Hill saturation is non-linear; linear-Gaussian SCMs are linear by construction. The bridge linearizes around the operating point (mean weekly spend per channel). The marginal coefficient at current spend is preserved exactly.

Why closed-form math, not Bayes Server runtime

The constructed SCM is fully linear-Gaussian. All three Pearl-ladder queries — observation, intervention, counterfactual — reduce to standard linear algebra and have exact closed-form posteriors. Component 3's R implementation matches what Bayes Server's exact inference engine would compute on the same .bayes file. The runtime isn't needed; the file is the auditable artifact.

For non-Gaussian extensions — Poisson sales, mixed discrete/continuous nodes, hierarchical pooling, full DBN unrolling for adstock — Bayes Server's runtime via rJava becomes the right backend. The current implementation doesn't need it. A future production version would.

Component 1 — Reader

bridge_reader.R

Parses the JSON written by Robyn's robyn_write() and produces a structured R object that downstream components consume. Defensive against Robyn version drift — uses Robyn::robyn_read() when available, falls back to jsonlite::read_json() otherwise. Field extraction handles both camelCase and snake_case conventions because Robyn's schema has shifted across releases.

The output BridgeInputs object exposes five sections: meta (model ID, adstock type, window), paid_channels (with coefficient, theta, alpha, gamma, ROI, calibration flag per channel), organic_channels, context_vars, and prophet_decomp. Plus a model-fit summary with nrmse, decomp.rssd, and R² values for diagnostic display.

Public API

# Read a Robyn fit JSON and extract bridge inputs read_robyn_fit(json_path) → BridgeInputs # Print a human-readable summary print(bridge_inputs) # Audit for missing fields before passing to Component 2 audit_bridge_inputs(bridge_inputs) → character vector of issues # Convert to a plain list (drops S3 class) for serialization bridge_inputs_to_list(bridge_inputs) → list

Defensive parsing — sample

The most fragile part of Component 1 is the per-channel summary extraction. Robyn 3.12.1 stores per-channel data in ExportedModel$summary as a data frame, but the column names changed at some point — older versions used rn for variable name, newer use variable. The reader handles both:

channel_summary <- function(ch) { # Find the row by variable name. Robyn 3.12.1 uses 'variable'; # older versions used 'rn'. Try both. name_col <- if ("variable" %in% names(summary_df)) "variable" else if ("rn" %in% names(summary_df)) "rn" else NULL if (is.null(name_col)) return(empty) row <- summary_df[summary_df[[name_col]] == ch, , drop = FALSE] if (nrow(row) == 0) return(empty) list( coef = pick("coef"), total_response = pick("decompAgg") %||% pick("xDecompAgg"), roi = pick("performance") %||% pick("roi_total") %||% pick("roi_mean"), boot_mean = pick("boot_mean"), ci_low = pick("ci_low"), ci_up = pick("ci_up") ) }

The %||% coalescing operator and the pick() helper that returns NA for missing fields keep the reader resilient: a JSON missing one field doesn't crash the whole pipeline, it just produces a BridgeInputs with that field as NA. The audit function then surfaces missing fields explicitly so Component 2 doesn't silently consume incomplete input.

Full file: R/bridge_reader.R · Documentation: docs/bridge_reader_README.md

Component 2 — SCM Constructor

bridge_constructor.R

Takes a BridgeInputs object and writes a Bayes Server .bayes file with the structural causal additions Robyn doesn't make: the latent confounder, the U-noise parents, the linearized media coefficients. Returns a BridgeSCM object containing the file path and the structural-vs-associational comparison.

XML is templated directly from R rather than calling Bayes Server's Java API via rJava. Tradeoffs: simpler setup (no Java dependency), but no Bayes-Server-side validation at write time. Validation happens when Component 3 loads the file for inference, or when the user opens it in Bayes Server desktop.

The structural correction formula

The associational-to-structural translation is parameterized as a linearized Gaussian back-door correction. For each paid channel:

At λ=0 the bridge agrees with Robyn (no confounder asserted). At λ=1 the bridge applies full back-door correction. Calibrated channels (those with experimental anchors) get attenuated lambda by 70% — the experiment partly blocks the back-door, so the correction shouldn't double-count.

Per-channel back-door strengths

Component 2 accepts latent_to_media as either a scalar or a named list. The named-list form lets the analyst specify different back-door strengths per channel — TV with 0.7 (advertisers heavily plan TV around demand forecasts) and Search with 0.0 (search is more demand-driven on the user side, less planning-driven on the advertiser side):

build_scm_from_robyn( bridge_inputs = br, output_path = "./robyn_outputs/bridge_scm.bayes", lambda = 1.0, latent_to_media = list( tv_S = 0.7, # upfronts-locked planning, strong back-door search_S = 0.0 # demand-bid auctions, weak back-door ), latent_to_sales = 0.5 )

This is the kind of judgment call a configurator playbook elicits during week 2 of a real engagement. The current implementation defaults to a uniform 0.7 across all paid channels for the demo dataset.

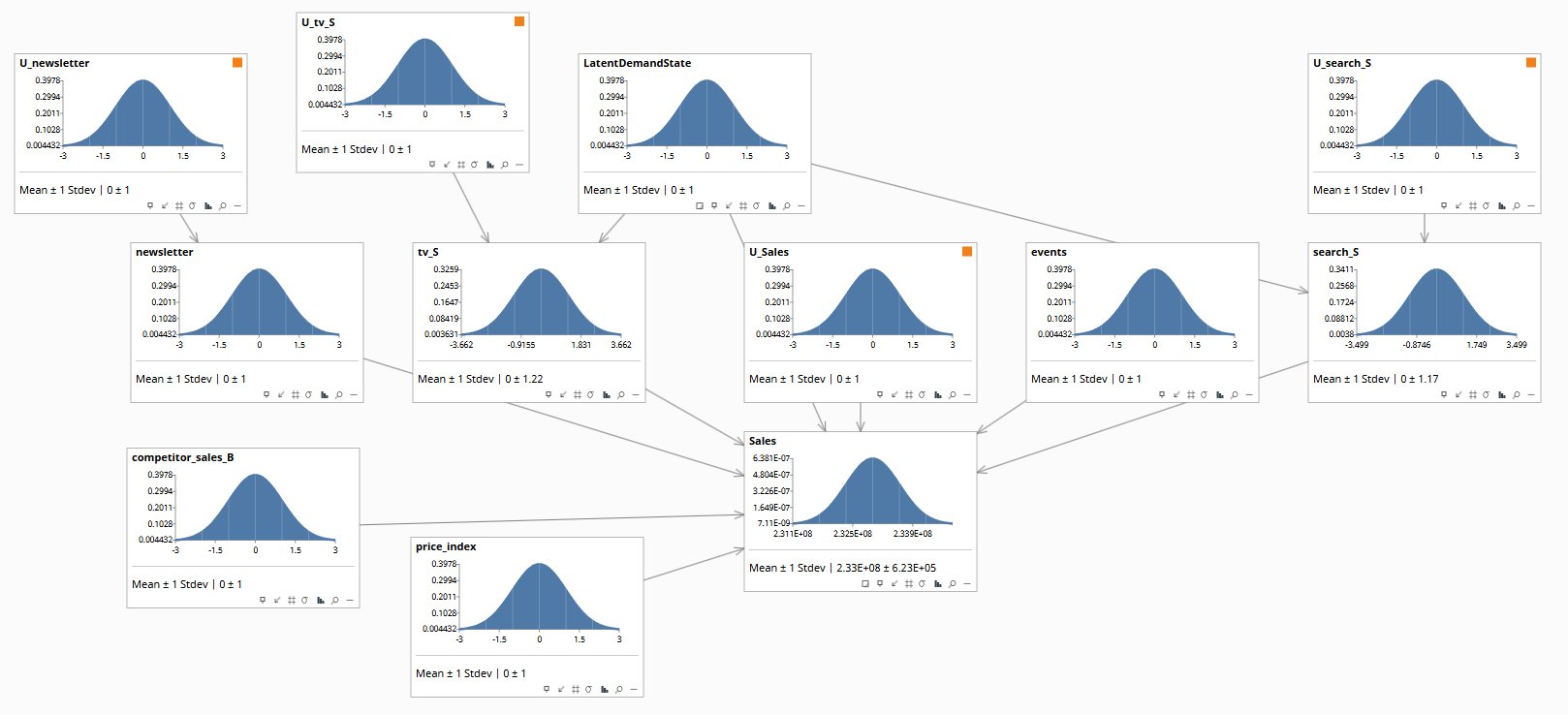

What gets emitted

The output .bayes file is a self-contained Bayes Server network. For the synthetic demo dataset (2 paid channels, 1 organic, 3 controls), it has 12 nodes and 13 links: the LatentDemandState root, U-noise nodes for each substantive variable, the Sales outcome with structural coefficients, and the context variables as observable inputs. The file is openable in Bayes Server desktop for independent inspection.

LatentDemandState sits at top — the back-door confounder Robyn doesn't model. Orange flags mark the U-noise parents required for Rung-3 counterfactual inversion. Media channels (tv_S, search_S, newsletter) receive arrows from both the latent and their U-noise. Sales at bottom-right shows the marginalized outcome (~$233M ± $623K at zero evidence), with structural coefficients on every incoming arrow. The latent-strength parameters driving the bridge's correction — latent_to_media per channel, latent_to_sales, lambda — are domain-elicited rather than measured. Elicitation is hard; the bridge doesn't eliminate the problem, it parameterizes it so the assumptions can be made explicit and sensitivity-tested via the Shiny app's sliders.Full file: R/bridge_constructor.R · Documentation: docs/bridge_constructor_README.md

Component 3 — Query Runner

bridge_queries.R

Runs the three Pearl-ladder queries against the constructed SCM, producing the corrected ROIs and counterfactual attributions that Component 4 renders. Implementation is closed-form analytic — every query reduces to standard linear algebra on the linear-Gaussian SCM. No Bayes Server runtime needed; the math is exact.

Also includes sweep_lambda() — rebuilds the SCM at a range of λ values and returns a tidy dataframe of structural ROIs across the sweep. This is the data the Shiny app's sensitivity-slider chart renders.

The three queries

Pearl's ladder distinguishes three classes of question, each requiring more structure than the last:

- Rung 1 — Observation.

E[Sales | observed(spend = X)]. The data-conditional expected Sales. What Robyn already reports. Component 3 reproduces it as a sanity check. - Rung 2 — Intervention.

E[Sales | do(spend = X)]. The structural effect of intervening on spend, with all back-door paths cut. The bridge's headline output. - Rung 3 — Counterfactual.

E[Sales* | observed evidence, do(spend* = 0)]. Per-campaign attribution. Given a specific observed period, what fraction of the lift is causally attributable to the campaign vs. would have happened anyway?

Closed-form computation — sample

The Rung-2 (intervention) query is the cleanest: do() cuts inbound arrows to the intervened node, so the latent demand state and other roots return to their unconditional means (zero), and only the direct structural effect contributes:

query_rung2 <- function(scm_rf, channel, do_value, structural_coef) { # In a do-intervention, all upstream paths to <channel> are cut. # The latent demand state and other roots return to their # unconditional means (zero), and only the direct structural # effect of <channel> on Sales contributes — at level # structural_coef * do_value. expected_sales <- scm_rf$base_sales + structural_coef * do_value list( channel = channel, do_at = do_value, expected_sales = expected_sales, expected_lift_per_dollar = structural_coef ) }

Rung 3 is more involved — it requires the abduction step (posterior on root variables given the observed evidence) followed by the action step (apply the intervention in a twin network) and the prediction step (compute the outcome). All three steps are closed-form for linear-Gaussian SCMs; the implementation is about 30 lines.

Lambda sweep — the sensitivity-chart data

sweep_lambda( bridge_inputs = br, output_dir = "./robyn_outputs/sweep", lambdas = seq(0, 1.4, by = 0.05), latent_to_media = 0.7, latent_to_sales = 0.5 ) → # tidy dataframe: lambda, channel, robyn_roi, structural_roi

This rebuilds the SCM and reruns Component 3 at 29 lambda values from 0 to 1.4. On a recent laptop the full sweep takes 1–2 seconds. The Shiny app calls this on every parameter change to refresh the sensitivity chart.

Full file: R/bridge_queries.R · Documentation: docs/bridge_queries_README.md

Component 4 — Shiny App

app.R

Single-file Shiny app that wraps Components 1–3 in an interactive front-end. Loads a Robyn fit at startup, exposes the causal assumptions as sliders (λ, per-channel latent_to_media, latent_to_sales), and renders three tabs: Headline (Robyn vs bridge bars), Sensitivity (lambda-sweep curves), Counterfactual (Rung-3 attribution).

Reactive expressions cache the SCM build and the lambda sweep so slider drag feels responsive. Export tab provides downloads of the constructed .bayes file, the audit table, and the lambda-sweep CSV. Deployable to shinyapps.io without any non-R dependencies.

The reactive graph

# On startup (cached for app lifetime) BRIDGE_INPUTS <- read_robyn_fit(ROBYN_JSON) # On every parameter change (slider drag) l2m_list <- reactive({ # Per-channel latent_to_media as a named list, from the dynamically # rendered per-channel sliders }) scm_current <- reactive({ build_scm_from_robyn(BRIDGE_INPUTS, tempfile(), lambda = input$lambda, latent_to_media = l2m_list(), latent_to_sales = input$l2s) }) queries_current <- reactive(run_bridge_queries(scm_current())) sweep_current <- reactive({ sweep_lambda(BRIDGE_INPUTS, tempdir(), lambdas = seq(0, 1.4, by = 0.05), latent_to_media = l2m_list(), latent_to_sales = input$l2s) })

Each plot's renderPlot() depends on either queries_current() or sweep_current(), so dragging a slider invalidates the relevant reactive and triggers a chart redraw. The cascade is automatic — Shiny handles the dependency graph.

What the analyst actually sees

Four tabs, each addressing one job:

- Headline. Side-by-side bar chart of Robyn ROI vs bridge structural ROI per channel, with truth lines (where known) for sanity. The single most important screen.

- Sensitivity. The lambda sweep — solid curves of bridge correction as λ goes from 0 to 1.4, dotted lines for Robyn's reported ROIs, vertical line marking current λ slider position.

- Counterfactual. Stacked bars decomposing observed weekly sales into "would have happened anyway" vs "campaign-attributable" for a high-spend week.

- Export. Download buttons for the current

.bayesfile, the audit CSV, and the lambda-sweep CSV.

Full file: R/app.R · Documentation: docs/app_README.md

app.R described above, deployed against a worked Robyn fit. The reactive graph is exactly what's shown in the code block: the SCM is rebuilt on every slider change, the λ-sweep is recomputed when the latent-strength inputs change, and each plot's renderPlot() tracks its upstream reactive automatically. Use the Headline tab to see the Robyn-vs-bridge ROI gap per channel, the Sensitivity tab to read the bridge correction across the full λ range, the Counterfactual tab for a Rung-3 high-spend-week decomposition, and the Export tab to download the constructed .bayes file and audit CSVs for independent inspection. Closed-form analytic posteriors against the linear-Gaussian SCM — mathematically equivalent to Bayes Server exact inference, no Java runtime needed in the deployment.Running it end-to-end

The full pipeline reproduces in roughly fifteen minutes on a multi-core laptop, ten of which are Robyn's hyperparameter search. Everything else is fast.

Prerequisites

- R 4.3+ with Rtools (Windows) or build-essential (Linux/Mac)

- Python 3.11+ for synthetic-data generation

- Robyn package:

install.packages("Robyn")— see Robyn's docs for full setup including the Python venv withnevergrad

Reproducing the worked example

# Generate synthetic dataset (Python) python python/build_mmm.py python python/build_robyn_dataset.py # Fit Robyn (R, ~10 min on a multi-core laptop) Rscript R/robyn_run.R # Run the bridge end-to-end (R, instant) Rscript -e ' source("R/bridge_reader.R") source("R/bridge_constructor.R") source("R/bridge_queries.R") br <- read_robyn_fit("./robyn_outputs/RobynModel-3_121_9.json") scm <- build_scm_from_robyn(br, "./robyn_outputs/bridge_scm.bayes", lambda = 1.0) print(run_bridge_queries(scm)) ' # Or launch the Shiny app Rscript -e 'shiny::runApp("R/app.R")'

Expected output

On the synthetic dataset, where the structural truth is knowable in advance, Robyn reports inflated TV ROI ($2.83 vs truth $2.00, +41%); the bridge recovers TV within 8% of truth at λ=1.0 with latent_to_media=0.7. Search shows the methodology's limit honestly: Robyn's regularization shrinks Search below truth, and the bridge can correct back-door bias but not regression shrinkage upstream. See outputs/mmm_three_rungs_analytic.txt in the repository for the closed-form analytic reference.

The bridge tool's headline result is genuine but partial: TV's bridge ROI lands within 8% of structural truth, demonstrating the methodology works. Search shows the limit — when Robyn's regularization shrinks a coefficient below truth (rather than above it), the bridge's downward correction overshoots. This isn't a bug, it's a real boundary of the bridge's value: it corrects for back-door confounding, not for upstream regularization choices in the regression itself.

A future extension would refit the model jointly under the SCM rather than layering correction on top of an already-shrunk fit. That's a different product — closer to "MMM with built-in causal structure" than "bridge tool over Robyn." A bigger build, a different methodology argument.

The repository

All four components plus the synthetic data, the standalone SCM, the Robyn fit script, and per-component documentation live in a single repository. MIT-licensed, open for clone, fork, or extension.

Repository structure

What's not in the repo (yet)

Three things a production version would need that the current implementation doesn't have:

- Joint refitting. The bridge currently corrects Robyn's already-fit coefficients. A more rigorous version would refit the model with the SCM structure baked in from the start, avoiding the regularization-shrinkage limit shown by the Search channel.

- Hierarchical pooling. Multi-geo, multi-brand, partial pooling — the bridge handles single-geo only. Hierarchical extensions are tractable but require more SCM structure.

- Non-Gaussian likelihoods. Poisson sales, truncated-normal spend, mixed discrete/continuous nodes. These break the closed-form math and require Bayes Server's runtime via

rJava— the right backend for production use.

Each of these is a real engineering project, not just a config knob. The current implementation demonstrates the methodology works on a synthetic linear-Gaussian dataset; production extensions are where the consulting engagement adds value beyond the open-source code.

If you want the methodology applied to your MMM, the engagement is described on the Strategy page. If you want to extend the code, the repository is on GitHub.

Email: info@rung3.ai